If you’d invested in one Bitcoin on January 1st, 2017—when the price was $1,000—then cashed it out before Christmas, you’d have earned nearly $20,000. Had you waited until the following Christmas, you’d have earned just over $2,500.

The Fall 2017 bull run chewed up and spit out the weak hands who bought in because the price was going up, then sold because it was going down. As many people lost fortunes as those who made them. Some people took away valuable lessons from that time, others internalized misinterpretations.

Cut to today. If you’d invested in one Bitcoin on January 1st, 2020—when the price was around $7,000—and kept hold of it until the time of this writing, you’d have made a healthy $40,000 profit.

The question now is: will 2017 repeat itself? Is this just another craze that, with a little pushback, will come back down to reality? Or will the price of Bitcoin just keep going up and up, leaving behind all the skeptics, all the folks who didn’t get in in time?

In other words: is it already too late to invest in Bitcoin?

There are two ways to answer this question, so let’s address them in turn.

Question #1: Will the Price of BTC Go Up?

This is what we all want to know, obviously. We all want to make money.

The thing is, when we ask this very general question—will the price go up—we actually mean something very specific. Translated, what we’re really asking is:

Will more Bitcoin be purchased than sold in the near future?

Supply vs. Demand

The price of Bitcoin goes up and down in accordance with natural supply and demand, with supply being relatively fixed. That makes the logic really simple. When more people are buying there’s less to go around, and sellers can command higher prices. When demand falls, sellers need to offer bargains. Which of these two scenarios are in our future?

While certain variables—like recent price movements, volume and options trading—can give some insight into near-future trends, there’s nobody who can say for certain what a ticker will do over the long run. If there were a foolproof logic to predicting Bitcoin’s price, anyone could throw their entire life savings into it (or, alternatively, into shorting it) and become a multi-millionaire.

Predictions

If you’re willing to gamble, though, there is evidence for and against buying now.

Some are predicting a BTC price correction, by the logic that...well...it has to come down at some point. 2017 is also a model for this view: that such violent gains aren’t sustainable long-term, and once everyone gets their heads back on straight they’ll surely cash out on their 2x and 4x gains.

But 2017 was characteristically different than 2020. It occurred when many people were just learning about Bitcoin for the first time, and lacked the kind of institutional support that kicked off this newest run. BTC optimists also point to their own historical trends—specifically, halvings—as evidence that Bitcoin will experience exponential growth past the six-figure mark.

Generally speaking, the optimists are winning out. The air around BTC right now seems to be bullish long-term, with an expectation of a modest pullback at some point in the coming months.

So if you’re willing to put your money where other people’s mouths are, it’s not too late to buy Bitcoin.

Question #2: Is BTC Undervalued or Overvalued?

Spend five minutes in the crypto space and you’ll find thousands of articles, millions of opinions, about Bitcoin’s price. In contrast, very few people are concerned with a related, arguably more important matter:

What is Bitcoin’s value?

Price vs. Value

If price and value seem like synonyms to you, you’re not alone. In reality, these are entirely different matters.

Price, as we’ve mentioned, is malleable. It goes up and down for logical and, often, illogical reasons.

Value is objective, inherent to the thing itself. It is not subject to the vicissitudes of investor sentiment.

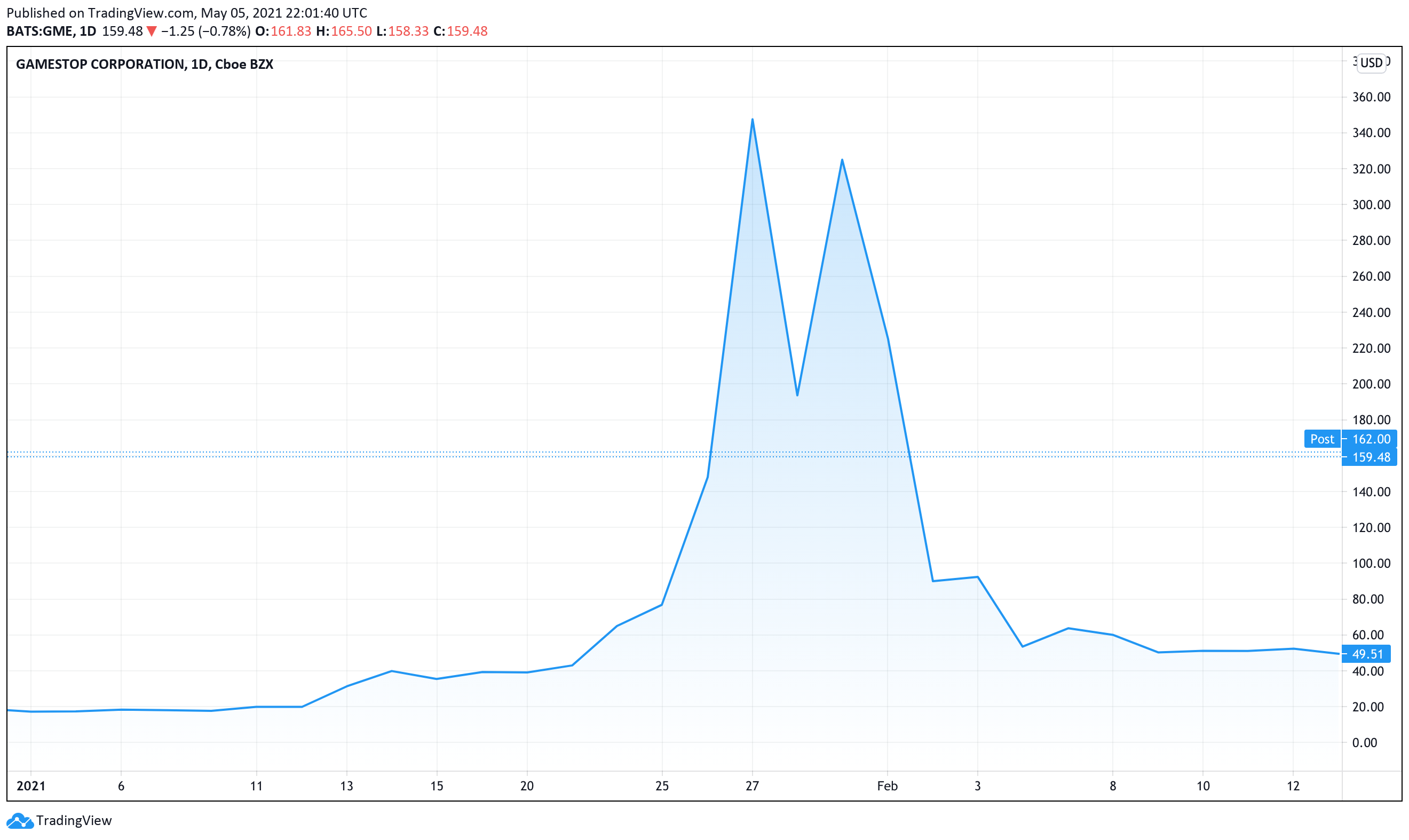

As an analogy, we can look to the recent Gamestop bonanza. Enterprising Reddit users cooperated to buy up Gamestop (GME) stock, driving its price to unbelievable highs.

Meanwhile, the underlying value of the company—its revenue, assets and so on—remained unchanged.

Most stocks won’t experience what GME did this January, but the underlying lessons remain. Namely:

- Price is fickle. In the short-term it may swing wildly back and forth according to psychological factors, or even intentional manipulation by moneyed interests.

- Value is price’s anchor—its magnet, applying constant force against those swings until, long-term, the two are married.

Bitcoin’s value, eventually—if not in one year, then 10, if not 10 then 100—will determine where its price ends up. So let’s talk about it.

Is BTC Like Traditional Assets?

Performing fundamental analysis to determine the intrinsic value of, say, Coca-Cola Company, isn’t simple, but it’s entirely doable. Investors do it every day. It involves examining their financial statements, then creating financial models to observe, analyze, and project income statements, cash flow, debt schedules, and also doing qualitative due diligence on the management team, et cetera et cetera.

Determining the fundamental value of Bitcoin is a rather different matter, because Bitcoin is unlike traditional asset classes.

- Bitcoin is simply computer code. It’s not something that you can hold in your hand, or use, like gold, or a Coke. Of course, many modern software companies sell code for a business, but they differ from Bitcoin in one crucial respect…

- Bitcoin’s code is run by thousands of independent computers around the world. You can visit Coca Cola’s factories, or gold mines, Amazon’s HQ or their AWS data centers, but there is no single Bitcoin “factory,” or HQ, or server farm. In theory, you could burn the biggest mining farm in the world, then 1,000 more after that, and the underlying network will remain entirely intact (it might slow down for a period of time, but that’s it). You can kidnap every core dev and their work will remain.

For these reasons, Bitcoin resists comparison with traditional corporate assets, and gold arguably even more so.

Instead, Bitcoin is often compared to fiat currencies—the U.S. dollar, Yen, etc. Yet here, too, we run into problems.

Is BTC Like Fiats?

Consider the U.S. dollar. A dollar is worthless in a vacuum—should the world collapse it can be used in a fire pit, or perhaps as toilet paper, but little else. It is valuable only so long as it’s backed by a stable, responsible treasury. Put another way: the dollar is only worth anything because we trust that it is, because the U.S. government inspires such trust.

Bitcoin, by contrast, is decentralized. It’s backed by no one in particular. Its form, its supply, and the mechanisms by which it operates were largely codified a decade ago by an anonymous individual or individuals who went MIA almost as soon as the network went public. Bitcoin’s codebase is maintained voluntarily by developers around the world with no contractual obligation to one another, or investors on the whole. The maintenance of the network is carried out by self-interested corporations and investors.

The word for all this is “trustless.” Bitcoin works not because you trust whoever’s behind it, but because you don’t have to; because there’s nobody to fill that position in the first place, yet the coins keep on moving.

In other words, Bitcoin may be a currency, yet it is the very antithesis of the U.S. dollar in spirit.

So if Bitcoin isn’t like a company, or gold, or a dollar, how do we determine what it’s actually worth?

Factors to Consider

Some have suggested that, even though Bitcoin is not like a company, there are certain checklists in traditional equity investing which apply to it nonetheless.

For example, Bitcoin’s white paper is a lot like a business plan: it describes what it is, how it works, how it might be used, and so on. Therefore, the white paper can be used as a kind of argument for whether Bitcoin’s prospects are good. Is it convincing in what it’s trying to say? Does it lay out a coherent and sustainable plan for the long-term? How has it held up in the last decade—has everything gone to plan, and what might that indicate for the next decade?

Here’s another parallel: while Bitcoin has no employees, it nonetheless has many people working on it at all hours of the day. There are its core developers who maintain the code, individual nodes which provide security, and miners who process transactions. All of these parties keep Bitcoin running. Is it a stretch, then, to analyze these parties in the way one would the management team or the employees of a traditional corporation? We might consider, for example, whether the core development team is competent, and what their rate of turnover is. We might consider the number of full nodes in the network and ask: does Bitcoin have enough people to ensure its security? We can look at mining pools to determine whether their centralization could threaten network performance in the future.

Other traditional investment metrics we might consider are:

- Target market - Who does Bitcoin attract, and who can it attract? Is there a future where everyone in the world owns cryptocurrencies, or will it forever remain the fodder of criminals, libertarians, techies and finance bros?

- Competition - What other cryptocurrencies might challenge Bitcoin’s market share? Plenty of altcoins have tried, or are currently trying. Is Bitcoin number one because it’s the best cryptocurrency, or because it possesses the most name recognition? What if something better comes along?

- Roadmap - The final Bitcoin will be mined over 100 years from now, but mining rewards will become minuscule long before that. Will transaction fees suffice to compensate miners—the people who process transactions over the network? Will it cause transaction fees to become overly expensive for users? In what other ways might Bitcoin change in the years to come, and what changes (or lack of change) might challenge its long-term viability?

- Regulation Risks - Because Bitcoin is controlled by no one, can go wherever the internet reaches, and is largely anonymous, no government can destroy it or totally prevent its use within their national borders (even taxing it is a chore). But plenty of governments have experimented with bans, China being the model. If countries start to make cryptocurrency trading illegal, for reasons good or bad, it won’t stop black markets but it will affect how many law-abiding citizens participate in the space.

- Distribution of shares - Plenty of companies are owned by majority shareholders. A startup CEO might own 100% of their company. The founders of a publicly-traded corporation might choose to hold onto 51% of its shares, so that they have the power to decide its future. Bitcoin simply can’t work like that. Bitcoin must be owned by the many, each in small part, or else the system is no longer trustless. An entity, or many entities together, representing over 50% of Bitcoin’s total supply can manipulate the market for their own short-term profit. That will never happen so long as Bitcoin’s total market cap remains so high, yet even a minority shareholder with enough stake can cause serious damage. For example, institutional investors with billions of dollars-worth of BTC could, theoretically, use their stake to pump and dump, artificially influencing the price for the entire market. So, if few-enough parties own enough Bitcoin, does that pose an issue for its long-term viability?

All of these are worthwhile factors to consider when determining the intrinsic value of Bitcoin. Yet none suffice to explain the most fundamental, most crucial question of all:

Why is Bitcoin worth anything in the first place?

Why is there Bitcoin?

There’s no risk that humans will stop drinking, therefore there will always be a market for companies like Coca Cola Co. The internet seems to have entrenched itself in society for the long term, therefore there will always be a need for software and data infrastructure, like Amazon’s AWS business and the products and services that run atop it.

In contrast, humans have traded with currencies for millennia, without any need for Bitcoin. So what’s to say this isn’t just a fad that we’ll all grow out of? How can we be sure that people will still want to own Bitcoin 5, 10 or 100 years down the line?

The fundamental reason for having a decentralized, digital currency was outlined at the very top of Bitcoin’s original white paper:

A purely peer-to-peer version of electronic cash would allow online payments to be sent directly from one party to another without going through a financial institution.

Why would this be important for ordinary people?

Commerce on the Internet has come to rely almost exclusively on financial institutions serving as trusted third parties to process electronic payments. While the system works well enough for most transactions, it still suffers from the inherent weaknesses of the trust based model. Completely non-reversible transactions are not really possible

[. . .]

Merchants must be wary of their customers, hassling them for more information than they would otherwise need. A certain percentage of fraud is accepted as unavoidable. These costs and payment uncertainties can be avoided in person by using physical currency, but no mechanism exists to make payments over a communications channel without a trusted party.

Bitcoin would take the power from banks (which, just a couple years prior, had proven themselves very untrustworthy), and put it back in the hands of individuals. It would mean less hassle and more privacy in financial transacting, and better protection against fraud.

Remarkably, all these years later, Bitcoin has come through on its promises. Anybody can buy Bitcoin anonymously right now, from anywhere in the world, so long as they have a computer with an internet connection. While many people choose to trust in third-party companies, nobody has to: you can have complete, guaranteed ownership over your investment. And, most remarkable of all: Bitcoin has proven more secure than any other asset in existence. It is infinitely easier to break into the Pentagon, for example, than it is to steal Bitcoin from a responsible investor.

So it’s safe to say that the vision for Bitcoin, laid out over a decade ago, has borne out. That’s good news, but it also doesn’t tell the whole story.

Use Cases

Even if Bitcoin has proven everything it set out to prove, does that necessarily mean that it is valuable for the reasons its founder thought it would be? This is a subtle but important distinction.

Bitcoin’s founder posited that, by creating a better system for people to pay one another, people would use it to...pay one another. Here’s the thing, though: while Bitcoin is traded every day (a lot), almost nobody actually pays with it. Another subtle yet important distinction.

Most Bitcoin transactions today are made in an investment context: buying and selling, as one would with corporate stocks or gold. It’s a distant memory now, but people used to imagine Bitcoin as something you could use like an actual currency—to buy food, for example. They turned out to be wrong.

People sometimes send crypto to friends and colleagues, but not nearly to the level they use Venmo or Paypal, for example. Outside the immediate crypto ecosystem, few conventional businesses accept Bitcoin as payment. (Even then, only in limited capacities. And, usually, it’s because that company believes BTC’s value will go up—a fundamentally different reasoning than what motivates them to accept fiat currencies.)

Why Bitcoin Isn’t Used for Payments

There are various technical hurdles that might have contributed to why Bitcoin never took off as a payment mechanism: the difficulty in accessing and securely transacting crypto on the go, for instance, and the fact that crypto is still too technical for most people to grasp. But, more than anything else, we can look to Gresham’s Law.

Gresham’s Law states that “bad money drives out good.” To understand what this means, imagine two gold coins: one made entirely of gold, the other half gold and half copper. Both coins may have the same face value—the same buying power in the market—but because one is made entirely of gold, you’ll more readily spend the one made with cheaper copper. Everybody with some full-gold and some half-gold coins will do the same, hence the pure coins will be hoarded and the cheaper will circulate. Bad money drives out good.

Imagine now, instead of gold coins of different quality, you have a dollar and a dollar’s-worth of Bitcoin. Which are you more likely to spend?

If you believe that Bitcoin will be more valuable in the future than it is today—which you almost certainly do, if you own it in the first place—you’ll hold onto it and spend the dollar. Thus, it is a contradiction to invest in Bitcoin and also use it to pay for things.

But this contradiction introduces a second, even more troubling contradiction.

If Bitcoin isn’t viable as a means of payment, then what is it actually good for?

Is Bitcoin Good for Nothing?

Unlike Amazon, Bitcoin doesn’t produce anything. Unlike a can of coke, it has no property (here, refreshment) that is valuable to a human being in and of itself. And unlike the U.S. dollar, you’d be operating against your own self-interest by using it to make purchases.

Bitcoin is, therefore, only worth buying if you’re going to sit on it, while more people decide to buy more of it later.

But this is a kind of house of cards, right? What happens if, eventually, enough people stop believing that the price will go up? In such a scenario, there is no supporting reason to hodl. For a community that values trustlessness, it can be a scary prospect: Bitcoin only has any value as long as we trust that other people value it as much or more than they do now.

(Even government currency, trust-based as it is, is highly useful—necessary, in fact, to the function of a modern society. So where any given currency may inflate out of existence as a result of one government’s failures, currencies in general are necessary to social order, and therefore possess an inherent value.)

Can BTC Be Worthless and Expensive?

That BTC recently jumped to multiples of where its price was just a few months ago is seen as evidence, by bulls, that the world is finally catching on to its value. But the same story can also be interpreted the exact opposite way: that only a fundamentally speculative asset, without a perceptible underlying value, can be worth $10K one month and $50K a few months later.

Bitcoin enthusiasts will argue that they’ve always believed this exponential growth was on the horizon. Fair enough. But is this belief based on objective fundamentals—properties of Bitcoin itself—or more subjective factors like general sentiment, or past behavior as a predictor for future performance (something tradfinance disproves time and again on broad-enough timescales)?

A good exercise here would be to try and calculate a specific valuation for what Bitcoin should cost, and why. Would it be adequately valued at $100,000? How about $1,000,000,000? The simple act of doing this mental exercise will help you narrow down your reasons for valuing Bitcoin, and the precise (not vague, not optimistic) degree to which you do.

The Future of Bitcoin

Much of the discourse today, particularly in light of the COVID-19 economy, surrounds Bitcoin as a hedge against more traditional assets, and currency inflation and debasement. Some of the more popular lines of reasoning go like this:

- Bitcoin has a defined, limited supply. Therefore, it has an advantage relative to almost all other currencies which experience constant inflation.

- Because it is decentralized and trustless, Bitcoin is not subject to the failures of untrustworthy and incompetent governments, nor the games played by those in the traditional financial sector.

- Bitcoin isn’t negatively correlated with the stock market in the way the dollar is, and sometimes the two trend in the same direction. But crypto does tend to have a mind of its own, and unpredictability can be a kind of protection when everything else is going one way.

- Bitcoin has performed far better than any other investment asset since its conception. So, to the extent that past history indicates future performance, it is worth getting at almost any time, no matter what.

Plenty of these arguments are well-founded and compelling. At least for the near-term, they may well bear out. None, however, address the nagging question that will have to one day be answered:

If it doesn’t produce any value, and it’s not viable as a currency, then why is Bitcoin worth anything instead of nothing at all?

Without a sufficient answer, there’s no telling whether it’s too late to get into Bitcoin. It’s a free-for-all. Have at it. Kill or be killed.

Written by Nathaniel Nelson for Knockaround.

New Netflix Shows We Can't Wait to See

9 Best Celebrity Podcasts